How to Read Your Credit Report and Understand Your Score

How to Read Your Credit Report

If you’re looking at a credit report for the first time it can be quite intimidating.

Your credit report may be a single document but it holds a lot of power in your life, from day-to-day activities to major milestones. It’s what helps you secure a mortgage, a credit card, a car loan and other credit products.

Your credit report is a report card on a certain aspect of your financial situation. It hands creditors, employers and anyone else you share it with a snapshot and history of how you manage your credit products and debts along with how you’re paying bills. It also lets them know how much debt you have and who you owe money to.

Do you know what your credit score is and how your credit report reads? Turns out, a whopping 56 percent of Canadians say they have never checked their credit score and only 14 percent check at least once a year, according to a recent Bank of Montreal survey.

Another 52 percent of Canadians don’t know what constitutes a good score. While 72 percent of Canadians know that lenders and financial institutions look at credit scores during the loan application process, 81 per cent of Canadians don’t realize that others — potential employers, insurance agencies, cell phone companies and landlords — also consider a potential candidate’s credit report, according to another poll.

With so much riding on your credit score, it’s important to get a concrete grasp on your credit report, your credit score and where you stand when it comes to debt management.

Here’s what you need to know about your credit report:

Why You Need to Pull Both Reports

Equifax and TransUnion are the two official credit reporting companies in Canada, and you should get your report from each of them. You may believe, like most Canadians, that both agencies report identical information, but they don’t! Some banks and lenders report to only one agency, some to the other, and some report information to both. Meanwhile some banks will rely on Equifax, some TransUnion, and others both. For these reasons, you need to know how you’re being portrayed on both reports.

Get a copy of both reports, and look through each of them carefully. They’ll outline all of your credit products, the debt you’re carrying on them, and if you’ve been late on any payments over the past 6 years. Keep a watchful eye for any errors or accounts that don’t belong to you. Believe it or not, one in four credit reports have errors. They’re usually small, but if you find one, it’s up to you to report it to either the creditor who is incorrectly reporting something or the credit bureau company. You’ll also need to follow up and make sure the error is ultimately corrected.

How to Understand Your Credit Score

A combination of factors make up your credit score, the single number that holds all the weight in your credit report. The factors include:

Payment history: ensuring you have a steady habit of making payments on time

Utilization ratio: the amount of credit you use divided by the amount of credit available to you (generally speaking, it is best to have a utilization ratio no more than 30 to 50 percent)

History of accounts: longstanding accounts are valuable as they show a lengthy history of being a good borrower

The number of inquiries you’ve made: seeking credit too often may make you look like a risky candidate

You can find out more about the key factors that are used to calculate your credit score. However, it’s good to be aware that your credit score can vary between credit bureaus and financial institutions. This can be because each credit bureau may have different information about your debts (not all companies report your debts to both credit bureaus) and because each bank often creates its own proprietary credit score that it requires its employees to follow when lending money. At the end of the day, though, all of these credit scoring systems are fairly similar. Each one just puts a little more or less emphasis on certain aspects of your credit history.

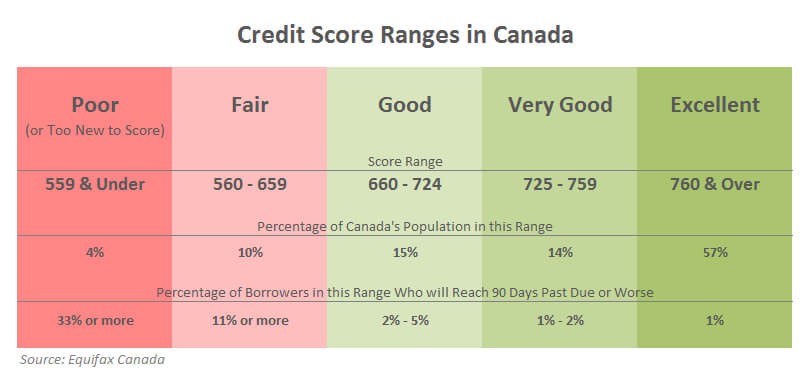

Generally speaking, your credit score is built on a range from around 300 to either 850 or 900 with higher scores representing a better mark. The report provides your score along with how you stack up next to other Canadians. A score between 725 and 759 is “very good.” Only 14 per cent of the Canadian population falls into this category. Other ranges on the scale include poor, fair, good, very good and excellent.

Take Any Advice or Pointers

Your credit report, right below your credit score, will outline precisely what’s dragging your score down. It will list three factors — in order of importance — to guide you on what you can do to improve your ranking. Read this section carefully.

Some examples of pointers include: Missed payments in the past two years, accounts going into collections, abusing your credit utilization ratio, opening too many accounts, or even not opening enough. There are hundreds of potential reasons that the report could generate.

Don’t be too discouraged if your credit score isn’t perfect. Keep in mind, your financial institution and creditors aren’t focusing solely on the number. They work in other internal factors, too, such as your client history and their own risk algorithms.

Triple Check Your Personal Information

It may be simple, but scanning through the personal information section is crucial. Make sure your full name, address, and date of birth is accurate, along with your social insurance number.

There may be a risk that your information could be linked to another person, especially if you share an identical name or a common name.

There could be two reports out there tied to you and you don’t know which one is making its way into your banker’s hands.

Your employment is listed, too. Anytime you apply for a credit product, you’re asked about your employment and income.

Study Your Accounts Closely

The meat of your credit report lies in your accounts and the stories they tell. Your credit report will list all of your accounts and your payment history, as reported to TransUnion and Equifax by your creditors.

Each account is listed, along with the type of credit it is. Revolving accounts, for example, are credit cards and lines of credit. Installments could be car loans and Open means accounts, such as cell phone accounts and utilities, in which your monthly bill isn’t a fixed amount.

Your report also states whether your account is an individual account you’re solely responsible for, if you’re a co-signer or if you’re sharing a joint account.

Zero in on your payment status. You want this section to say “Paid as agreed.” If you’re missing payments, make sure it’s not a mistake on your creditor’s end. And try to rectify the issue by getting back to making payments on time.

This part of your report may point to banking information but there will only be data here if you have an overdraft account that’s gone delinquent or into the hands of a collection agency. Your credit report will never state how much you have in your bank account.

Accounts reported to these agencies will stick around on your record for years — Equifax, for example, holds onto records of accounts for six years. If you have a credit card debt that’s five years old, for example, it may be better to leave the account untouched than to pay the debt and let it linger for another six years.

How Many Credit Inquiries are You Making?

Whenever you ask for a loan or a new credit product, the potential lender will pull your credit report to see how trustworthy you are. These requests for your credit report will show up in this section — it’ll detail the date, the requestors’ organization and their contact information.

Nothing should look unfamiliar in this section. If your credit report is being pulled without your knowledge, this could be a red flag for fraud.

Consumer Statement and Public Notices

This final section of your report will document any consumer proposals, bankruptcies and other judgments against you on your accounts in the past six years. After the time is up, your job is to make sure the debts are removed from your report and you have a clean slate again.

Consumer statements are any messages you’d like to convey on your credit report. You could explain why there’s a mark on your report. Your explanations could vary: maybe you’ve been a victim of fraud, you had a family emergency that’s caused your payments to go into arrears a few years ago, or you’re in the process of correcting an error, for example.

You could even note that you’re in a debt repayment plan and getting back on track with your finances to communicate to them that you’re a responsible consumer.

<< Back to the Blog main page

Worried about your credit?

Get answers from an expert.

Whether it’s about keeping, building, or rebuilding your credit, we can help if you’re feeling overwhelmed or have questions. One of our professional credit counsellors would be happy to review your financial situation with you and help you find the right solution to overcome your financial challenges. Speaking with our certified counsellors is always free, confidential and without obligation.

Hi Chris, neither Equifax nor TransUnion provides a score on your credit report. You can get scores from them by paying for their corresponding services, but please keep in mind that different lenders use different credit scoring systems and that any score you see will only be an estimate of what a lender might use.

ERS stands for Equifax Risk Score. They are providing you with version 1.0. This is the credit score calculation that Equifax provides for educational purposes. There is also version 2.0, and some online lenders claim to use it. The bottom line with your score is that no credit reporting agency is going to provide you with your real score – even when you pay for it (the US government fined a number of credit reporting agencies for not fully disclosing this a number of years ago). Only lenders get your real score. The public is only ever provided with an estimate of their score using a different calculation. The truth is that you only need a general estimate of your score because it’s just an estimation of how likely you are to repay your debt.

So – said a different way when you Equifax sends a report with all its detail – (I just received one) we can’t find out our credit score?

Hi Chris, neither Equifax nor TransUnion provides a score on your credit report. You can get scores from them by paying for their corresponding services, but please keep in mind that different lenders use different credit scoring systems and that any score you see will only be an estimate of what a lender might use.

I got an Equifax report. I cannot find any information about the “ERS 1.0”. My ERS 1.0 has and “x” underneath it. What does that mean?

ERS stands for Equifax Risk Score. They are providing you with version 1.0. This is the credit score calculation that Equifax provides for educational purposes. There is also version 2.0, and some online lenders claim to use it. The bottom line with your score is that no credit reporting agency is going to provide you with your real score – even when you pay for it (the US government fined a number of credit reporting agencies for not fully disclosing this a number of years ago). Only lenders get your real score. The public is only ever provided with an estimate of their score using a different calculation. The truth is that you only need a general estimate of your score because it’s just an estimation of how likely you are to repay your debt.