How to Rebuild Your Credit in Canada – 7 Points

What’s a good credit rating in Canada?

Your credit score is your ticket to qualifying for a loan, securing a credit card or locking in a good interest rate on a mortgage. While your credit score is just a number, it’s an invaluable indicator that lets banks and lenders know you’re responsible with your finances.

Turns out, Canadians may not be aware of how important a good credit score is and how much of your daily life it can affect. Most Canadians don’t realize just how ubiquitous their credit score is, touching many important facets of their daily lives, according to a national poll. An employer may check your credit score when being considered for a job and insurance companies and cell phone companies might look at credit scores during the application process, too.

Your credit score is even looked at if you’re a small business owner hoping to get approved for a small business loan.

But you can hurt your credit score in many ways — from missing credit card payments, maxing out your credit cards or defaulting on loans. In other severe instances, you could be starting from scratch after you have filed for bankruptcy or a consumer proposal.

No matter what your situation, there is a way to rebuild your credit regardless of how severe your predicament may be. It just takes time, dedication and persistence as you prove to lenders that you’re a trustworthy consumer.

Here are A Handfuld Of Ways You Can Rebuild Your Credit in Canada

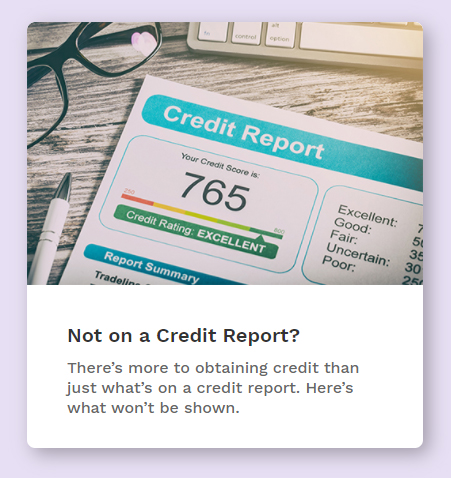

Check Your Credit Report

A good habit to adopt is to check your credit report annually through the credit reporting agencies Equifax and TransUnion. It’s like your report card to see how you’re faring with your various creditors.

If you’re trying to rebuild your credit, looking at your credit report is a good first step to learn what you’re doing wrong and where you stand with your accounts.

Look at your credit score — a score between 725 and 759 is “very good” and only 14 per cent of the Canadian population falls into this category. Your score will range from “poor” to “excellent” depending on where you fall from 300 to 900.

An additional important thing to pay attention to is the part on the report where it lists three factors that explain what you can do to improve your credit score.

Take Care of Any Late or Outstanding Payments

Your credit report will list all of your credit products, from credit cards to loans, along with how you’re paying bills. You’ll notice if you’re falling behind on accounts, if some are going into collections, or if there is anything that is incorrect on your report.

If there are any issues, the onus is on you to fix them. If you’re behind on anything, play catch up, make your payments, and commit to stay on top of them to reverse the situation.

This applies to your cell phone bills, too. Believe it or not, companies report this to the credit bureaus as well – along with utility bill payments that are way past due.

If you’re in dire straits, you may need to pick up the phone to call your creditors to explain any issues and work out a solution, or speak with a credit counselling organization like ours to see how to resolve things in a way that will work for you.

Open a Secured Credit Card

When you’re seen as a risk to lenders, qualifying for something as simple as a credit card can be an uphill climb. Your best bet is to open a secured credit card, in which you’ll put down an upfront security deposit that will equal or exceed your credit card limit.

Use this card responsibly and diligently pay the minimum balance at the very least. This step will help you rebuild your credit.

Play by the Rules

One major component of your credit score is your payment history. Making payments past the due date or missing them altogether doesn’t put you in lenders’ good books.

Make sure that you always keep your accounts in good standing by making payments on time, paying down your debts and ensuring that your credit utilization ratio isn’t too high.

Your credit utilization ratio is how much of your credit you’re using out of the total amount of credit available to you. If you want the best score possible, try not to use more than 30 per cent.

So if you have access to $10,000 on a credit card, keep your balance below 30 per cent or $3,000. Anything above that may begin to cause your credit score to slip. The credit scoring system takes into account your credit utilization as a whole but also for each credit product you have.

Creditors may look at your credit utilization ratio and how much credit you’re carrying on cards and see you as a risky client. Maxing out any form of credit can also been seen as a sign of greater risk and will definitely have a negative impact on your credit score.

If you struggle with paying your bills on time, try setting up an automated bill payment each month. This way you’ll know you won’t miss a payment. Once you’ve shown consistency with your payment history, you’ll lay the groundwork to show you’re responsible with your credit.

If your finances are too tight right now to setup automatic payments, you’d likely benefit from sitting down with one of our Credit Counsellors. They can help you put together a realistic budget and see what all your options are to improve your finances and start making progress toward your financial goals.

Go Slow, Start Small and Have Patience

Credit isn’t destroyed overnight. It takes time. In the same way, repairing damaged credit often isn’t quickly either. Rebuilding credit is a process that takes time.

If you started from ground zero and built up a good history with a secured credit card, it may be time to graduate to an unsecured credit card. Commit to a small limit though and only use the card for purchases you know you can pay off. Don’t rush home and pay off your purchases immediately. Instead, wait until you receive your statement, and pay it off in full before the due date.

Use this time to study your spending habits and how you damaged your credit score in the first place. Were you overspending, too forgetful to make payments or you buried your head in the sand as credit card statements came in?

Acknowledge what went wrong so you can ensure you won’t be a repeat offender as you’re working hard to rebuild your credit.

Limit Your Credit Inquiries

While you may be tempted to get your hands on credit, you need to make this a slow and steady rebuilding process. Each time you ask for a loan or a new credit product, your credit report will be pulled.

Multiple inquiries on your report could be a red flag to creditors — it’s suggesting you’re taking on credit too hastily so be aware and space out your inquiries accordingly. Opening too many accounts could hurt your score, too so be selective and open one account at a time.

Hang Onto Longstanding Accounts

There are merits to hanging onto a long-established credit card account, especially one that you’ve kept in good standing. It helps to increase the average age of your accounts.

Get Help

Rebuilding credit is an arduous task that involves many moving parts from budgeting, managing creditors, and cleaning up accounts that could have fallen into collections.

If you’re inundated and don’t know where to start, contact a certified, non-profit credit counsellor to help you sort through your finances. A certified, non-profit credit counsellor can help you in several ways, depending on your needs. Some of the services they provide include assisting in building a debt repayment plan, negotiating lower interest rates with your creditors, and creating a budget with debt repayments to help you stay accountable.

Last Updated on January 10, 2025